Life throws curveballs, doesn’t it? One minute you’re cruising along, and the next, you’re hit with an unexpected expense—a car repair, a medical bill, or maybe you’re just trying to consolidate some debt. Whatever the reason, sometimes you need to borrow money, but nobody wants to drown in high-interest payments. Finding where to borrow money with low interest can feel like searching for a needle in a haystack, but it’s not impossible. In this guide, I’ll walk you through the best options, share insider tips, and help you make smart choices to keep your wallet happy. Let’s dive in!

Why Low-Interest Loans Matter

Before we get into where to borrow money with low interest, let’s talk about why it’s such a big deal. Interest rates can make or break your financial health. A loan with a high interest rate might seem manageable at first, but over time, those extra percentages add up, leaving you paying way more than you borrowed. Low-interest loans, on the other hand, keep your payments affordable and help you pay off the principal faster. Plus, they’re easier on your budget, giving you room to breathe. So, where can you find these unicorn-like loans? Let’s explore the top spots.

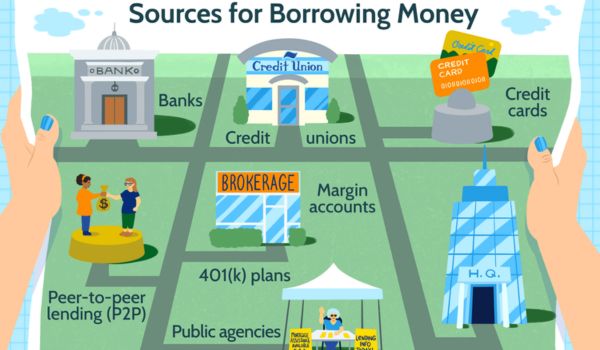

1. Credit Unions: Your Friendly Neighborhood Lender

If you’re wondering where to borrow money with low interest, credit unions should be at the top of your list. Unlike big banks, credit unions are member-owned, which means they’re all about serving you, not just making a profit. Because of this, they often offer lower interest rates on personal loans, auto loans, and even mortgages.

To get started, you’ll need to join a credit union, but don’t worry—it’s usually pretty easy. Many credit unions have loose eligibility requirements, like living in a certain area or working in a specific industry. Once you’re a member, you can access loans with rates that are often 1-2% lower than traditional banks. For example, in 2025, some credit unions offer personal loans with APRs as low as 5-7%, compared to 10% or more at big banks. Plus, they’re more likely to work with you if your credit isn’t perfect. Check out local credit unions or national ones like Navy Federal or Alliant to see what they offer.

2. Online Lenders: Convenience Meets Competitive Rates

The internet has changed the game when it comes to borrowing money. Online lenders like SoFi, LendingClub, and Prosper are shaking things up by offering low-interest loans without the hassle of visiting a brick-and-mortar bank. These platforms are a great place to borrow money with low interest because they operate with lower overhead costs, which means they can pass the savings on to you.

What’s cool about online lenders is how fast and easy the process is. You can apply in minutes, get pre-approved, and compare rates without leaving your couch. Many of these lenders also cater to people with good credit, offering rates as low as 4-6% for personal loans. If your credit score is above 700, you’re in a prime position to snag a great deal. Just be sure to read the fine print—some online lenders charge origination fees that can bump up the overall cost. Compare multiple offers to find the best fit for your needs.

3. Banks: Traditional but Still Competitive

Don’t count out traditional banks just yet. While they might not always have the lowest rates, many banks offer competitive loan options, especially if you’re already a customer. Banks like Chase, Wells Fargo, and Bank of America often provide low-interest loans to people with strong credit histories or existing accounts. If you’re wondering where to borrow money with low interest, your current bank might be a good starting point.

One perk of borrowing from a bank is the relationship factor. If you’ve got a checking account, savings account, or credit card with them, they might offer you a loyalty discount on your loan’s interest rate. For instance, some banks knock off 0.25-0.5% if you set up automatic payments from your account. Rates for personal loans at banks typically range from 6-10%, but you might score a better deal if you shop around. Pro tip: Check if your bank offers secured loans (like a home equity loan), which often come with lower rates because they’re backed by collateral.

4. Peer-to-Peer Lending: Borrowing from Real People

Peer-to-peer (P2P) lending is a lesser-known but awesome option for borrowing money with low interest. Platforms like Funding Circle and Upstart connect borrowers directly with individual investors who fund your loan. It’s like cutting out the middleman, which can lead to lower rates and more flexible terms.

Here’s how it works: You apply through a P2P platform, and investors decide whether to fund your loan based on your credit profile and story. If you’ve got a solid credit score (say, 680 or higher), you could qualify for rates as low as 5-8%. P2P lending is also great if you need a loan for something specific, like starting a small business or covering a big purchase, because you can explain your situation to potential investors. Just watch out for platform fees, which can add 1-5% to your loan cost. Still, P2P lending is a solid choice if you’re hunting for low-interest options.

5. Government-Backed Loans: A Safety Net for Specific Needs

Sometimes, the government has your back when it comes to borrowing money with low interest. Programs like FHA loans, VA loans, and USDA loans are designed to help people afford homes, while other federal programs offer low-cost student loans or small business loans. These loans are backed by the government, which reduces the risk for lenders and keeps interest rates down.

For example, if you’re a first-time homebuyer, an FHA loan might let you borrow with an interest rate as low as 3-4%, even if your credit isn’t stellar. VA loans, available to veterans and active-duty military, often have even lower rates and no down payment requirements. If you’re a small business owner, check out the Small Business Administration (SBA) for loans with rates starting at 6-8%. The catch? These loans often have strict eligibility rules, so make sure you qualify before applying. If you do, they’re some of the best places to borrow money with low interest.

6. Family and Friends: A Personal Touch with Low (or No) Interest

Okay, this one might feel a little awkward, but hear me out: Borrowing from family or friends can be one of the cheapest ways to get money. If you’ve got a trusted loved one who’s willing to help, you might be able to borrow money with low interest—or even no interest at all. This option works best for smaller amounts or short-term needs, like covering a bill until your next paycheck.

The key here is to treat it like a real loan. Put the terms in writing (amount, repayment schedule, and any interest) to avoid misunderstandings. You can even use a platform like Loanable to create a formal agreement. Borrowing from family or friends can save you a ton on interest, but it’s not without risks—money can strain relationships if you’re not careful. Only go this route if you’re confident you can repay on time.

- How to borrow money from Cash App

- How to apply for a home equity loan

- Personal loan for debt consolidation

7. 0% Interest Credit Cards: A Short-Term Win

If you need to borrow a smaller amount and can pay it off quickly, a 0% interest credit card might be your ticket. Many credit cards offer introductory periods (usually 12-18 months) where you pay no interest on purchases or balance transfers. This is a fantastic way to borrow money with low interest—well, no interest—for a limited time.

Cards like the Chase Freedom Unlimited or Citi Diamond Preferred often come with these offers, especially if you have good credit (a score of 670 or higher). Just make sure you pay off the balance before the introductory period ends, because regular APRs can skyrocket to 15-25%. Also, watch out for balance transfer fees, which are usually 3-5% of the transferred amount. If you’re disciplined, this is one of the smartest ways to borrow money with low interest for short-term needs.

8. Home Equity Loans and HELOCs: Tapping into Your Home’s Value

If you own a home, you’ve got a powerful tool for borrowing money with low interest: your home’s equity. Home equity loans and home equity lines of credit (HELOCs) let you borrow against the value of your home, often at rates far lower than personal loans or credit cards. In 2025, home equity loan rates typically range from 4-6%, while HELOCs might start at 5-7%.

The upside? These loans are secured by your home, so lenders are willing to offer lower rates. The downside? If you can’t repay, you risk losing your home, so this option isn’t for everyone. It’s best for big expenses, like home renovations or debt consolidation, where you need a large sum and can handle steady payments. Shop around with lenders like Rocket Mortgage or your local bank to find the best rates.

9. Employer-Sponsored Loans: A Hidden Gem

Did you know some employers offer low-interest loans as an employee benefit? If you’re employed, check with your HR department to see if this is an option. These loans are often designed to help with things like emergency expenses or education costs, and they come with super low rates—sometimes as low as 2-4%.

The cool thing about employer-sponsored loans is that they’re usually deducted directly from your paycheck, so you don’t have to worry about missing payments. They’re not super common, but if your company offers this perk, it’s one of the best places to borrow money with low interest. Just make sure you understand the terms, like what happens if you leave your job before the loan is repaid.

10. Nonprofit Organizations: Help When You Need It Most

If you’re in a tough spot financially, nonprofit organizations and community programs might be able to help. Groups like the United Way or local charities sometimes offer low- or no-interest loans to people facing hardship. These programs are often small-scale, designed for things like utility bills or medical expenses, but they can be a lifesaver.

To find these options, search for “nonprofit loans near me” or contact your local community center. You might also check with religious organizations, as some offer financial assistance to members. While these loans might not cover huge amounts, they’re a great way to borrow money with low interest when you’re in a pinch.

Tips for Scoring the Lowest Rates

No matter where you borrow money with low interest, a few strategies can help you get the best deal possible:

- Boost Your Credit Score: Lenders reward high credit scores with lower rates. Pay down debt, make payments on time, and check your credit report for errors before applying.

- Shop Around: Don’t settle for the first offer you get. Compare rates from multiple lenders to find the lowest one.

- Consider Secured Loans: Loans backed by collateral (like your car or home) often have lower rates than unsecured loans.

- Negotiate: Some lenders, especially credit unions and banks, are open to negotiating terms if you’ve got a strong financial profile.

- Avoid Payday Loans: These come with sky-high interest rates (sometimes 400% APR or more) and can trap you in a cycle of debt.

Things to Watch Out For

Borrowing money with low interest is awesome, but there are a few pitfalls to avoid. First, watch out for hidden fees, like origination fees, prepayment penalties, or late fees, which can make a “low-interest” loan more expensive than it seems. Second, be realistic about what you can afford—borrowing more than you need can lead to trouble down the road. Finally, steer clear of predatory lenders who promise low rates but tack on outrageous terms. Always read the loan agreement carefully and ask questions if anything seems off.

How to Choose the Right Option for You

With so many places to borrow money with low interest, how do you pick the right one? Start by asking yourself a few questions:

- How much do you need? Smaller amounts might be best handled with a 0% credit card or a loan from a friend, while larger sums might call for a home equity loan or bank loan.

- How’s your credit? Good credit opens up more low-interest options, while fair or poor credit might point you toward credit unions or government-backed loans.

- How fast do you need the money? Online lenders and credit cards are quick, while home equity loans or government programs might take longer.

- What’s the purpose? Some loans, like SBA loans or FHA loans, are designed for specific needs, so make sure the loan matches your goal.

Once you’ve got a clear picture, compare offers and choose the one with the lowest total cost (interest plus fees) that fits your timeline and budget.

A Word on Economic Trends in 2025

As of April 2025, interest rates are influenced by economic conditions. The Federal Reserve has been adjusting rates to manage inflation, which affects loan rates across the board. While mortgage rates are hovering around 4-5% for qualified borrowers, personal loan rates range from 5-15%, depending on credit. Staying informed about rate trends can help you time your loan application for the best deal. Check resources like Bankrate or NerdWallet for up-to-date rate comparisons.

FAQS

Direct Subsidized Loans: You won’t be charged interest while you’re enrolled in school or during your six-month grace period. Direct Unsubsidized Loans: Interest starts accumulating from the date of your first loan disbursement (when you receive the funds from your school).

These loan apps with the lowest interest in Nigeria also offer quick accessibility to funds and legal compliance, among other perks.

FairMoney. FairMoney operates as a mobile bank for financial inclusivity. …

OKash. …

Aella Credit. …

QuickCheck. …

Carbon.

Simple interest loans are commonly used for short-term loans or consumer loans, such as personal loans, auto loans, or small business loans. These loans are often preferred for their straightforward and predictable payment structures, making it easier for borrowers to plan their finances and ensure timely repayments.

Conclusion

Finding where to borrow money with low interest doesn’t have to be a headache. Whether you’re tapping into a credit union, exploring online lenders, or even asking a family member for help, there are plenty of ways to get the funds you need without breaking the bank. The key is to do your homework, compare your options, and choose a loan that aligns with your financial goals. By focusing on low-interest options and avoiding common pitfalls, you can borrow smart and keep your finances on track. So, what are you waiting for? Start exploring these options today and take control of your money!